Collections Temporarily Delayed

On January 16, 2026, the Department of Education announced that it was temporarily delaying collection of defaulted student loans, but we don’t know how long the pause will last. If your loans are in default when the delay ends, you could face serious consequences, including losing your tax refunds, a portion of your wages, and even some of your Social Security benefits. The government can take these steps without going to court, and there is no statute of limitations to collect this debt. Take steps now to make sure your loans aren’t in default! If you are in default, act quickly to get out of default and avoid collections.

Did you get a notice that your loans are in default?

After your loans go into default, you may receive different notices telling you to take action to avoid collections. Don’t ignore these notices. If you do, the government can take steps to collect what you owe. You usually only have a limited time to act before collections start.

Read below for what to do if you get these different kinds of notices.

- An Email or Letter from Your Loan Servicer That Your Loans Just Went Into Default (“Last Chance” Notice)

- A Notice from the Department of Education (Initial 65-Day Notice or “Welcome to Default” Letter)

- A Notice from a FFEL Loan Guarantor or Other Collection Agency

1. An Email or Letter from Your Loan Servicer That Your Loans Just Went Into Default (“Last Chance” Notice)

If you miss payments on federal student loans, your servicer should contact you to help you get back on track. After nine months of missed payments, your loans are technically in default. Your servicer may send a “last chance” notice warning that your loans will be transferred to a default servicer if you don’t act fast. If your loan is still with your servicer and hasn’t been transferred to a default servicer yet, they might be able to reverse the default.

If you get this notice, call your servicer right away. On the call, you should ask to get your loans back into good standing and ask:

- to apply for an income-driven repayment (IDR) plan, or

- for a retroactive forbearance to bring your loan current.

Once your loan is back in good standing, make a plan to keep up with payments going forward.

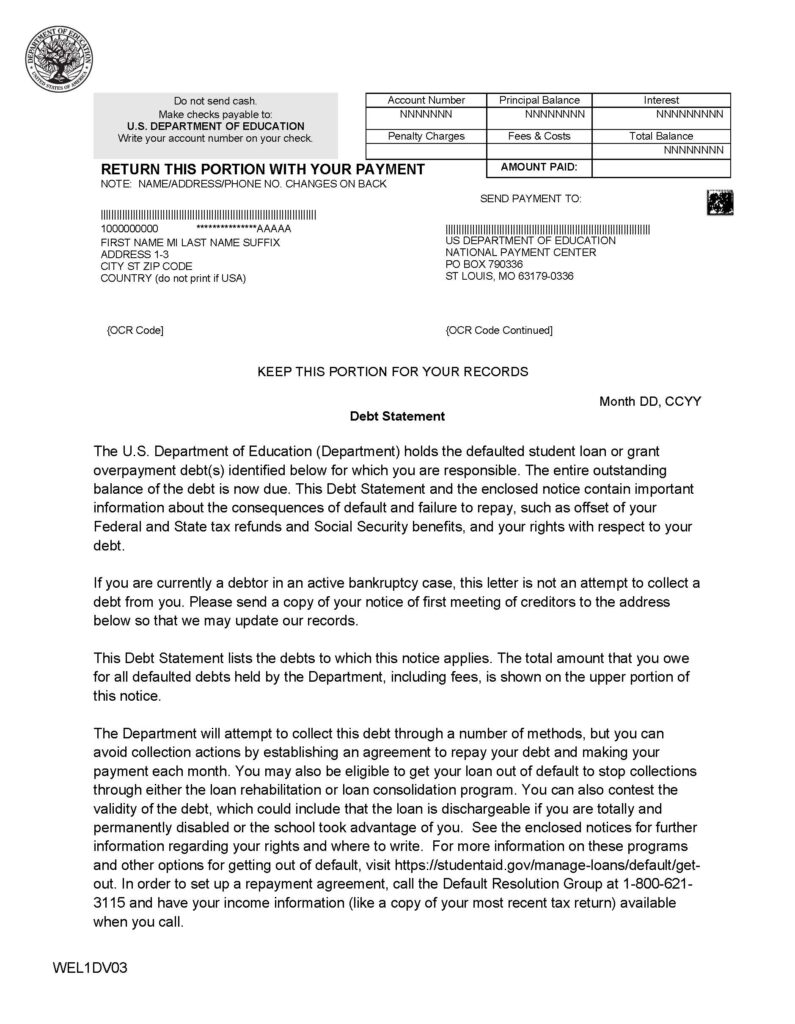

2. A Notice from the Department of Education (Initial 65-Day Notice or “Welcome to Default” Letter)

Shortly after your loan is transferred to a default servicer, you should get a notice telling you that your loan is in default. The notice gives you a short window (65 days) to act before collections start. The notice is several pages long. Included at the end of the notice is a “Request for Review” form with check boxes you can use to respond. If you act within 65 days, you may be able to stop collections from starting.

See the most recent example of what the Initial Default Notice looks like.

Warning: The government usually won’t send you another notice before taking part of your tax refund if you don’t act within 65 days.

What to do if you get the initial 65-day notice:

Option 1: Take Steps to Get Your Loans Out of Default

You can avoid collections if you do any of the following within 65 days to get your loans out of default:

- Submit a loan consolidation application

- Enter a rehabilitation agreement and make one payment

- Pay the loan in full

Option 2: Submit a Request for Review Form

If you can’t remove your loans from default, you can try to raise objections to stop collections from happening. The notice includes a “Request for Review” form that allows you to tell the Department of Education why you think collections shouldn’t occur.

See an example of the Request for Review form at the end of the Initial Default Notice.

On the form, make sure to explain why you believe your loans are not in default or why collections should not happen. Indicate whether you want a review based only on what you submitted in writing on the papers or if you would also like an in-person or telephone hearing. Generally, regardless of which option you choose, the decision is based on what you include with the form. It is very important to include all the reasons why you think your loan should not be in default and all supporting documentation when you submit the form.

The form asks you to check the boxes for the objections you wish to raise. Some common objections include:

- you already repaid the loan;

- the loan isn’t yours;

- you filed for bankruptcy, and it is still open, or the debt was discharged; or

- other valid reasons why you do not owe the money.

You can also raise an objection if you have a pending application for a discharge or cancellation program. You can apply for many types of discharge and cancellation programs even if your loans are in default, including:

- total and permanent disability discharge;

- closed school discharge;

- false certification or identity theft discharge; and

- borrower defense

You can apply for a discharge when you receive the 65-day notice and then raise your pending application as an objection to stop collections from starting. If you applied for relief before you received the notice, you can raise your pending application as an objection as well. When you send in your request for review, attach a copy of your cancellation or discharge application and include the date you submitted it.

3. A Notice from a FFEL Loan Guarantor or Other Collection Agency

If you borrowed loans before 2010, you may have a Federal Family Education Loan (FFEL) with a different lender than the U.S. Department of Education. If you received a notice from a company saying it is acting as a guarantor on behalf of the Department of Education, then you may owe a FFEL loan that is in default. You still have the same rights and options as borrowers with defaulted loans held (owned) by the Department of Education, but you may be dealing with different companies.

If you think the notice might be fraudulent or you don’t owe any FFEL loans, call the Default Resolution Group at 1-800-621-3115 to confirm that you have loans in default and who to contact.

Notice of Wage Garnishment: If you received a notice that the government is going to garnish your wages to collect defaulted student loans, visit our page on Administrative Wage Garnishments.

Notice of Social Security Offset: If you received a notice that the government is going to take a portion of your Social Security benefits to collect your defaulted student loans, visit our page on Social Security Offset.