On July 1, 2026, a number of changes to student loan borrowers’ options will go into effect. How you are impacted by these changes depends on your situation —whether you’re currently in school, in repayment, or planning to borrow for school in the future. Parents who take out student loans for their children’s education will also be impacted.

This article discusses what you need to know and what options you’ll have after July 1, 2026, including:

- What is changing on July 1?

- How is the new income-driven repayment plan, RAP, different from other repayment plans?

- How is the new Tiered Standard Plan different from other plans?

- I am currently repaying federal student loans. What do these changes mean for me?

- I borrowed Parent PLUS loans for my child’s education — will I be impacted?

- I want to borrow federal student loans to go to school in the future.

- I am currently in school. What do these changes mean for me?

It is more important than ever to have a plan for student loan repayment so that your loans do not go into default. Navigating all of the changes can be challenging, but the Student Loan Borrower Assistance Project is here to help, with guidance on understanding your loan situation, repaying your loans, loan forgiveness and cancellation programs, and postponing payments when you need time to figure out a plan.

What is changing on July 1?

On July 1, 2026, new rules on student loan repayment options and borrowing limits will go into effect. That will:

- Add a new income-driven repayment plan option, called the Repayment Assistance Plan (RAP), which will be available for most borrowers.

- Create two separate repayment tracks for Direct Loan borrowers, with different repayment options depending on whether the borrower took out any new loans (or consolidated existing loans) on or after July 1, 2026:

- Existing borrowers who took out all of their loans before July 1 will keep most of their existing repayment options – for now – and will add the new RAP option. Many existing borrowers can continue with their current repayment plans. But the SAVE plan is being eliminated, and the new rules will eliminate the PAYE and ICR plans in July 2028.

- Borrowers who take out any new loans on or after July 1, or who consolidate their existing loans after July 1, will only have two potential options: the new RAP plan or the new Tiered Standard Plan.

- End the Grad PLUS loan program (a type of loan for graduate and professional schools that previously allowed students to borrow up to the full cost of attendance) for any borrowers starting a program on or after July 1.

- Place new limits on how much students and parents can borrow in federal student loans, with limited exceptions for students who are currently enrolled and took out loans before July 1. These changes will primarily impact graduate and professional students and parents who take out loans for their children’s education.

In addition, borrowers enrolled in the SAVE plan will start receiving notices that they must switch to a different repayment plan because the SAVE plan is ending. For more on the end of SAVE, read our article on what borrowers in SAVE need to know.

How is the new income-driven repayment plan, RAP, different from other repayment plans?

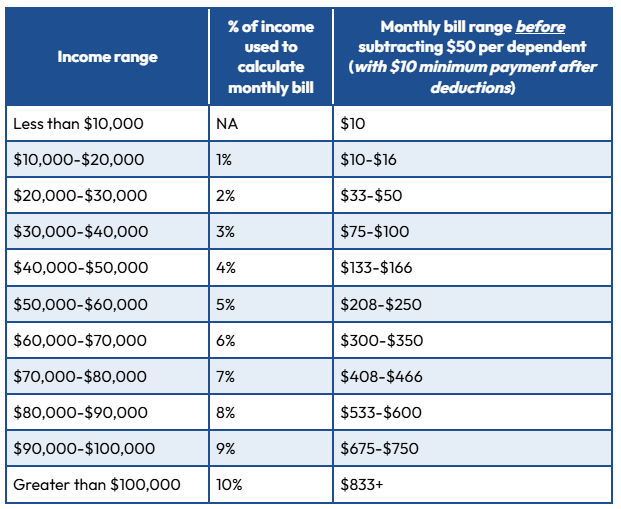

On July 1, the Department of Education will begin allowing Direct Loan borrowers to enroll in RAP, a new income-driven repayment (IDR) plan that calculates borrowers’ monthly payments off of a percentage of their income and cancels any remaining balance after 30 years of repayment. As in other IDR plans, payments in RAP will count towards Public Service Loan Forgiveness (PSLF).

Who is eligible?

All Direct Loans taken out for your own education are eligible for RAP. (Parent PLUS loans and consolidation loans containing Parent PLUS loans are not eligible.)

How are payments calculated?

Monthly payments will be calculated as a percentage of the borrower’s total income (using adjusted gross income, or AGI) minus $50 per month per dependent, with a minimum $10 payment:

What makes RAP different?

RAP has some important pros and cons that are different from the existing income-driven repayment plans.

Pros:

- Your loan balance will always decrease while you’re in the RAP plan and making on-time payments because any interest that accrues during a month that is not paid off via your monthly payment will be waived (canceled). In addition, if your monthly payment does not reduce your principal by at least $50 on its own, the government will reduce your principal by up to $50.

- Many borrowers will be able to pay off their loans sooner in RAP than in other IDR plans and will pay less in total over time.

Cons:

- Your monthly bill may be more expensive than it would be in the other IDR plans, particularly if you took out your loans after 2014, are low income, high income, or have a spouse or children. The RAP plan uses a very different repayment formula than the other IDR plans, and all borrowers must pay a minimum of $10 a month, no matter how little they make.

- Your maximum repayment period until you qualify for forgiveness of any remaining loan amount will be longer. In the RAP plan, you will not qualify to have your loans forgiven until you have made 30 years of payments, unlike 20-25 years in the other IDR plans. (However, most borrowers will repay in full before reaching 30 years, and will stop making payments then.)

- Time in RAP will not count towards forgiveness in the IBR plan. This means that if you eventually want to switch to IBR, you may have more years until you reach forgiveness.

For some borrowers, the benefits of a steadily decreasing loan balance and a potentially faster payoff may outweigh the risk of higher payments and a longer wait for loan forgiveness. To compare your potential IDR options, visit our page on all of the IDR plans and check out Federal Student Aid’s Repayment Calculator.

How is the new Tiered Standard Plan different from other plans?

A new fixed repayment plan, the Tiered Standard Plan, will also become available on July 1, 2026, but it will only be available to borrowers who take on at least one new loan after that date. This is the plan borrowers’ Direct Loans will automatically be placed in if they take out loans after July 1, 2026 and do not request the RAP plan.

Who is Eligible?

You must borrow a new loan after July 1, 2026, or consolidate your existing loans, to be eligible for the Tiered Standard Plan. Only Direct loans are eligible.

How is the Tiered Standard Plan different?

Like the old Standard plan, this plan generally requires the same payment every month and is designed to pay off a borrower’s loan in full by the end of their repayment period. But under the new Tiered Standard Plan, borrowers’ repayment periods will be based on their total outstanding Direct loan amount and will vary from 10 to 25 years.

That means many borrowers will have a longer repayment period in the Tiered Standard Plan than in the Standard plan for pre-July 2026 borrowers. Borrowers can always make extra payments to pay off their loans faster.

Other things I should be aware of?

Time spent in the Tiered Standard Plan will not count towards Public Service Loan Forgiveness.

To compare all of your repayment plan options, visit our page on repayment plans. To see what your monthly bill would be on the other plans, visit the Federal Student Aid’s Repayment Calculator.

I am currently repaying federal student loans. What do these changes mean for me?

If you are currently repaying federal student loans, the changes that take effect on July 1, 2026 might not impact you.

The changes on July 1, 2026 will only impact you if:

- You are enrolled in the SAVE plan and need to enroll in a new repayment plan. Starting on or after July 1, 2026, borrowers enrolled in the SAVE plan will be forced to pick a new repayment plan. If you are enrolled in SAVE and do not take out a new loan or consolidate any loans after July 1, 2026, you will be eligible for IBR and the new RAP plan, among other options for existing borrowers. You can learn more about the end of the SAVE plan in The SAVE Plan is Ending: What Borrowers in SAVE Need to Know.

- You take out a new loan or consolidate after July 1, 2026. If you take out even one new loan, or consolidate any of your existing loans, you will lose access to your current repayment options. Instead, you have to repay all of your Direct Loans in either the Tiered Standard plan or the RAP plan. You should consider whether you can afford payments in these plans before consolidating or taking on any new federal student loans.

- You want to access the benefits of the new RAP plan. All Direct loans for your own education are eligible for the RAP plan starting July 1, 2026.

- You owe Parent PLUS loans borrowed for your child’s education. More information on Parent PLUS loans is in the next section.

If you only have loans from before July 1, 2026, you will continue to have the same access to the existing IDR plans, IBR, ICR, and PAYE, as well as the Standard, Graduated and Extended plans. But, the ICR and PAYE plans will end on July 1, 2028, and if you are in ICR or PAYE, you will have to switch plans when they end.

I took out Parent PLUS loans for my child’s education — will I be impacted?

The July 1 changes will have a dramatic impact on many parents who took out Parent PLUS loans to pay for their child’s education. The impact will depend on whether you have already consolidated your Parent PLUS loans and whether you take out any new loans.

- If you consolidated your Parent PLUS loans before July 1, 2026, and you do not take on any new loans after July 1, 2026, then you can pay your Consolidation loan in an income-driven repayment plan if you enroll in IDR before July 1, 2028. Generally, you will have to enroll first in the ICR plan, and then after one payment you can switch to the IBR plan. If you do not switch out of ICR before the plan ends on July 1, 2028, you will be automatically switched to IBR then.

- If you did not consolidate your Parent PLUS loans before July 1, 2026, then you will not be able to repay them in an income-driven repayment plan. Your options will be limited to fixed repayment plans like the Standard or Extended plan, or, if you consolidate or take out a new loan after July 1, to the new Tiered Standard plan.

- If you consolidated your Parent PLUS loans before July 1, 2026, but you take out any new loans (or consolidate loans) after July 1, 2026, then you will not be eligible to repay any of your Parent PLUS loans (or Consolidation loans that repaid Parent PLUS loans) in an income-driven repayment plan. Instead, you will have to pay them in the new Tiered Standard plan.

- If you are planning on borrowing at least one Parent PLUS loan after July 1, 2026, then your options to repay it will be limited. Any Parent PLUS loans borrowed after July 1, 2026 will only be eligible for the Tiered Standard Plan. Additionally, after July 1, the amount that you will be able to borrow in Parent PLUS loans will be more limited.

Some people have loans for their own education, as well as Parent PLUS loans for their children’s education. If you have both types of loans, you can still repay loans for your own education in an income-driven repayment plan even if your Parent PLUS loans are not eligible. You will just have to repay your Parent PLUS loans in a separate plan, and you should not consolidate them with loans for your own education. If you consolidate your own loans with any Parent PLUS loans, the entire consolidation loan will need to be repaid in the Tiered Standard plan.

I want to borrow federal student loans to go to school in the future.

If you aren’t already enrolled in school, but want to go to school and take out loans in the future, your options will be more limited. Many students who go to school after July 1, 2026, will not be able to borrow as much in federal student loans as students who attended school before that date. This applies to students who go to school for the first time, return to school after stopping a prior program, or return to school for a new program. This change will primarily impact people who go to graduate or professional school and families that rely on Parent PLUS loans (loans taken out by parents for their children’s education).

Generally, if you enroll in a program after July 1, 2026:

- There are new limits on how much students can borrow for graduate and professional education. If the Department of Education considers a program to be a “graduate” program, you can borrow up to $20,500 per year and a total limit of $100,000. If you’re in a “professional” program, you can borrow up to $50,000 per year and a total limit of $200,000.

- There are no more Grad PLUS loans — a loan type for graduate and professional programs that previously could cover up to the full cost of attendance.

- There are new limits on Parent PLUS loans. Parents can only borrow up to $20,000 per child per year, and a total of $65,000 in Parent PLUS loans per child.

- Borrowers will be subject to a lifetime loan limit of $257,500 for any federal student loans ever borrowed, excluding Parent PLUS loans. This limit will apply regardless of whether any of those loans were paid off or canceled.

In addition, when it comes time to repay your new student loans, you will be limited to only two options: the Tiered Standard Plan and the RAP plan. (Parent PLUS borrowers will be limited to only the Tiered Standard Plan.) If you already have Direct Loans, then taking out new loans will change your repayment options on all of your Direct Loans. You will lose access to the existing repayment plans and will only be able to repay your Direct Loans in the Tiered Standard Plan or the RAP plan.

I am currently enrolled in school. What do these changes mean for me?

If you are currently enrolled, both the new loan limits on how much you can borrow and the changes to repayment options could impact you.

Loan Limits

If you are currently enrolled in school and took on at least one federal student loan for the program you are enrolled in before July 1, 2026, then the graduate and professional loan limits discussed above will not apply to you while you are completing your program. But, if you switch programs or switch schools, you will be subject to the new loan limits.

The new limits on Parent PLUS loans will not apply to you if you are currently enrolled in school and either took out a Direct loan before July 1, 2026 or your parent took out a Parent PLUS loan for you before that date for the program you are currently enrolled in. But the limits will apply if you switch schools, withdraw, or complete your program. The limit will not apply to you if you switch majors within the same degree.

Repayment Options

If you are enrolled in school and take on a new loan after July 1, 2026, all of your Direct Loans will only be eligible for the RAP plan or the Tiered Standard plan, discussed above, even if you took out some loans for your program before July 2026. Current students are not exempt from the repayment changes.