On January 16, 2025, the U.S. Department of Education announced that federal student loan borrowers can now, for the first time, see how many months of progress they have toward having any remaining balance on their loans cancelled through the Income-Driven Repayment (IDR) plans. Borrowers can see this information by logging in to their Federal Student Aid account at studentaid.gov. Borrowers should consider taking screenshots or otherwise save records of their IDR qualifying payment counts in case this information is ever disputed or removed from studentaid.gov.

Below, we cover:

- What IDR qualifying payments counts and payment terms are, and why they matter.

- How borrowers can check their IDR progress and save copies to protect their progress.

- How the one-time payment count adjustment helped fix past errors that prevented borrowers from getting as much IDR qualifying credit as they should.

What are IDR qualifying payment counts and payment terms, and why do they matter?

Income-Driven Repayment (IDR) plans were designed to offer borrowers an affordable option to repay their loans. IDR plans generally set monthly payment amounts based on the borrower’s income and family size each year. Additionally, because some borrowers will not make enough to fully repay their loans, even after paying for 20 years or more, IDR plans offer a “light at the end of the tunnel” – a requirement that after a certain amount of time in repayment, any remaining balance on the loan will be cancelled. The new tool on studentaid.gov shows the borrower their IDR payment term, how many qualifying months of payments they have made, and how many more months of qualifying payments they must make before the outstanding balance on their loans will be cancelled. Here’s what each of these numbers mean.

Most IDR plans have a 20 or 25 year “payment term,” meaning that after 20 or 25 years of qualifying monthly payments (i.e., 240 or 300 monthly payments) any remaining balance on the loan will be cancelled. You can learn more about the payment terms of each of the IDR plans here.

The SAVE plan, created by the Biden Administration in 2023, offers shorter payment terms – between 10 and 19 years – for people who borrowed less than $21,000 in federal student loans, including most community college students. However, the SAVE plan is currently tied up in the courts following legal challenges led by Missouri and Kansas, and Republicans members of Congress have recently listed cutting the SAVE plan and raising student loan payments as a potential way to pay for proposed tax laws.

“Qualifying payments” mean monthly payments, or certain other repayment statuses, that count toward reaching the end of the IDR payment term and qualifying to have any remaining balance cancelled. Months with the following payments or statuses are considered qualifying payments:

- full, on-time payments in any of the IDR plans (including the SAVE plan, REPAYE plan, PAYE plan, IBR plan, and ICR plan), including months where the borrower owed $0 in their IDR plan

- full, on-time payments in a 10-year Standard plan,

- all time in the COVID-19 Payment Pause,

- time in some types of deferments or forbearances or deferments

IDR qualifying payment counts show the number of months of qualifying payments the borrower has already made toward the total number of qualifying months required for cancellation through the IDR program. Similarly, the time until the end of the IDR payment term shows how many more years and months of qualifying payments the borrower will have to make until they qualify to have any remaining balance cancelled.

Example: Ava is enrolled in the PAYE plan and has a 20-year IDR payment term, meaning any remaining loan balance will be cancelled after she makes a total of 240 qualifying monthly payments. Ava has been making qualifying payments on her loans since January 2013 and now has an IDR qualifying payment count of 144 (12 years of 12 monthly payments). Ava has to make 8 more years of qualifying payments (96 more qualifying payments) until she reaches the end of her IDR payment term and any remaining balance is canceled.

Importantly, some borrowers will pay off their loans before the end of their IDR payment term. Because IDR payments are set based on income rather than on the loan amount, some borrowers end up fully repaying their loans in IDR plans before the end of the IDR payment term. Once the borrower has repaid their loan balance in full, the loan is paid off and they do not have to make any more payments, even if there is more time left in their IDR payment term. Additionally, borrowers who work in public service may be eligible for loan cancellation after 10 years of qualifying payments through the Public Service Loan Forgiveness (PSLF) program.

How can borrowers check their progress toward having any remaining loan balance cancelled through IDR?

To check your progress toward reaching the end of your IDR payment term and having any remaining balance on your loan cancelled, take the following steps:

- Log into your federal student aid account on studentaid.gov.

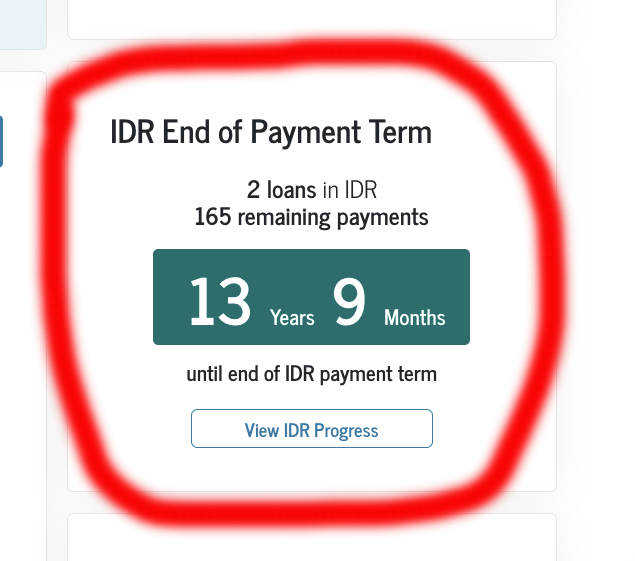

- You should now see your “student aid dashboard.” On the right hand side of the screen, there is a new section showing you how much time is left until the End of IDR Payment Term. This is how many more years and months of qualifying payments you will need to make before you qualify to have any remaining balance on your student loans canceled. Below is an example of what you are looking for on your dashboard:

- Consider taking a screenshot and saving it to your files, or printing the page to PDF and saving it to your files. This could be useful if the Department of Education stops presenting or updating this information on studentaid.gov, or if you have a dispute with your servicer or the Department about your qualifying time toward loan cancellation.

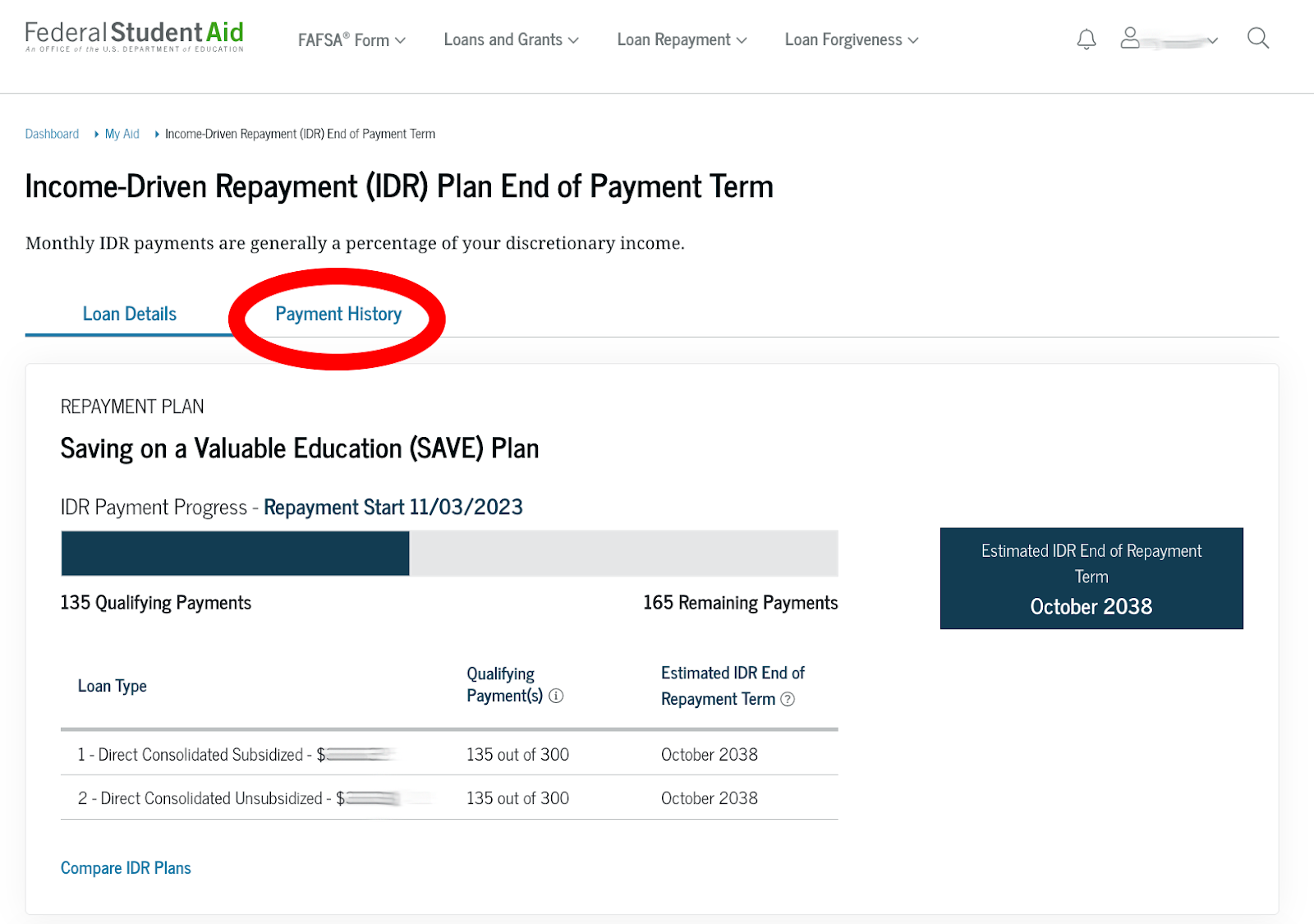

- Next, click on “View IDR Progress,” which will take you to a page where you can see your qualifying payment count for each of your federal student loans. Under “Qualifying Payment(s)” you will see, for each of your loans, how many qualifying payments you have already made toward qualifying to have the remaining balance of your loan cancelled via IDR. Again, consider saving screenshots, or printing to PDF and saving to your records. An example is below:

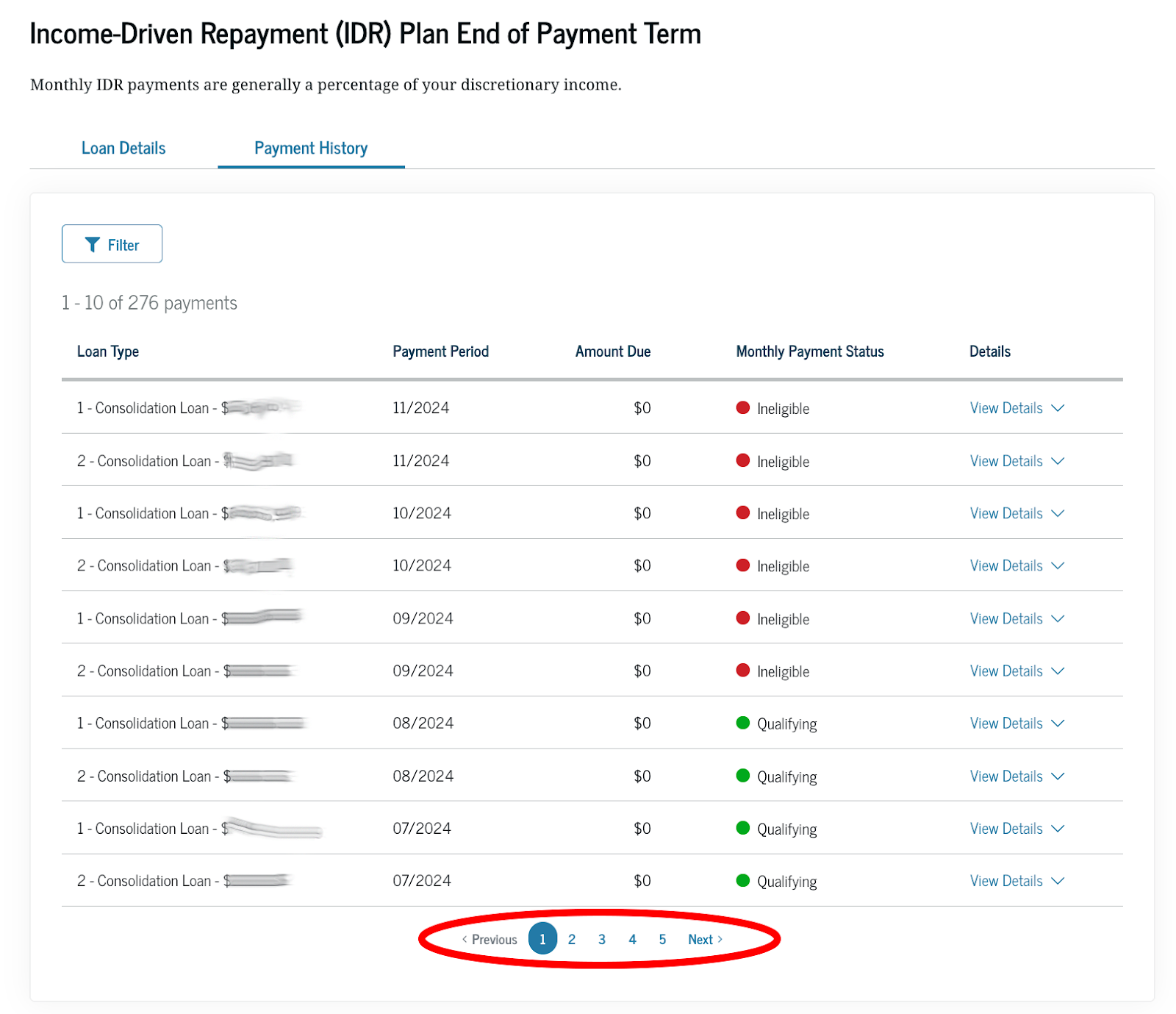

- Next, click “Payment History.” This page will show you for every month since you started repaying each of your loans, whether the Department has recorded that month as a “qualifying” payment month toward your IDR payment term, vs “ineligible.” An example is below. If you click on the filter, under “Payment Status” you can select not qualifying to see all of the months that have been marked ineligible on each loan. Look for any months marked as “ineligible” that you think might be a mistake. If you find any errors, consider filing a complaint and request for correction with the FSA Ombudsman. And again, consider saving screenshots or PDFs of the full payment history for each of your loans for your records. Only ten entries show at a time, so make sure you take a picture of each page of eligible and ineligible payments.

How did the one-time payment count adjustment impact qualifying payment counts and IDR progress?

The newly visible IDR payment counts reflect adjustments made under the one-time payment count adjustment (also known as the “IDR Account Adjustment”) first announced in 2022. For many borrowers, these adjustments increased their qualifying payment count by correcting for past servicing and record-keeping errors that prevented borrowers from getting as much qualifying time toward reaching IDR cancellation as they would have if the system was working.

The one-time payment count adjustment was completed in phases, and has already helped the 1.45 million borrowers who qualified to have their loans cancelled through IDR plans over the last four years. Previously, only 50 (!) borrowers had their loans cancelled through IDR plans.

The Department of Education announced on January 16, 2025, that it had largely completed the one-time payment count adjustment, and that the qualifying payment counts now viewable on studentaid.gov reflect the adjustments to borrowers’ accounts.

For more information about the one-time payment count adjustment, see here.