By: Kyra Taylor & Kat Welbeck

The promise of the Public Service Loan Forgiveness (PSLF) program is simple. Student loan borrowers who dedicate ten years to working in public service while paying off their student loans should have their remaining federal student loan balances cancelled. However, as evidenced by countless borrower stories and investigations, the promises of the PSLF program are not the reality for millions of public servants. At every turn, borrowers have been let down and buried under debt due to mismanagement and abuse by the Department of Education (ED) and the student loan industry.

The COVID-19 pandemic has laid bare the disgraceful failings of this program. While countless frontline workers upheld their commitments to their communities, ED failed time and time again to uphold its end of the bargain and denied these borrowers loan relief. Indeed, instead of correcting for years of misinformation spread by federal loan servicers and making relief easier to obtain, public servants pursuing loan relief must jump through countless bureaucratic hurdles and extensive delays before they are able to obtain the cancellation they are entitled to.

Legal aid providers are a part of the army of people who work every day to lift up our nation and their communities. Each year, they save millions of Americans from hardship, homelessness, and financial disaster. During the pandemic, they have been on the frontline protecting renters from eviction and homeowners from foreclosure, ensuring that families have access to health insurance and public benefits, protecting low-income workers’ labor rights, advocating on behalf of consumers, and helping to expand fair and equitable access to justice. Legal aid programs are often the first stop for Americans facing a survival crisis, but as legal aid employees have struggled with their own student loan debt, ED has failed to show up for them. ED must restore the promise of PSLF.

Legal aid workers have already begun standing up to share their stories and drive policy change. You can join them and submit your PSLF comment to ED here.

Legal aid attorneys, paralegals, managers, and administrative staff are speaking up about the failure of PSLF

The PSLF program has been plagued by issues since its inception; notably, 98 percent of public service workers who have applied for debt cancellation through the program have been rejected. A range of servicing abuses have knocked borrowers off track. Servicers have pushed borrowers into ineligible payment plans, miscalculated borrowers’ PSLF-eligible payments, mishandled records and payments, and steered borrowers into forbearance.

In July 2021, ED published a notice and request for information seeking public comment on issues related to the mismanagement of PSLF. In the three weeks since launching this public inquiry, ED has received nearly 10,000 comments from affected student loan borrowers and other stakeholders, including many from those working in legal services.

These borrowers’ stories make clear that the consequences of errors and breakdowns surrounding PSLF go far beyond a simple rejection rate. Their debt impacts every aspect of their lives and their families’ lives, causing some to delay marriage, children, or homeownership. Their student debt feels like a punishment for serving their community, and it forces them to stretch an already meager salary further. Here are a few examples of the challenges and hardships legal services providers have shared with the Department of Education via public comment:

Hear legal aid attorneys’ stories:

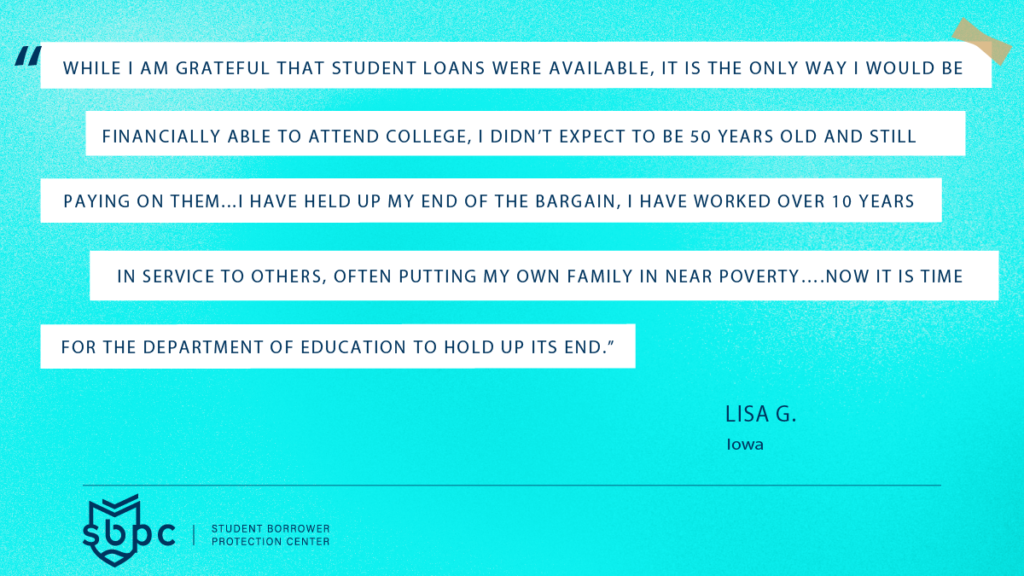

Lisa G: I worked multiple jobs to put myself through college because my family was not in a position to help me….While I am grateful that student loans were available, it is the only way I would be financially able to attend college, I didn’t expect to be 50 years old and still paying on them. I am currently paying on my loans while I am also trying to put my children through college so they don’t get into the debt cycle that I have endured.

I started my career as an attorney for Legal Aid representing the indigent making $31,000 with $160,000 in student loan debt. I had two children at the time and lived in subsidized housing because I couldn’t afford housing myself. For the next 15 years I worked for non-profit agencies…When I

inquired about PSLF with my provider, Mohela, they told me there was nothing I had to do (annual certification of your employment was optional) and once I reached 120 payments I should notify them to start the forgiveness process. Because of my low salary, my initial payments were $0, but I was told under the program they still counted towards the 120 payments. A couple of years later I decided I should go ahead and do the employment certification which resulted in my loan being transferred to Fed Loan.

Currently my account says I have 102 eligible payments, and 60 that are not eligible….Trying to get proper accounting of my payments has been a nightmare. At each turn I am met with barriers and challenges….I have held up my end of the bargain, I have worked over 10 years in service to others, often putting my own family in near poverty….Now it is time for the department of education to hold up its end.

Nicole H.: There are many problems with the Public Service Loan Forgiveness Program. I have been a Public Defender for almost 10 years. However, I will not qualify for loan forgiveness for another 5 years because several of my payments did not count since I was in the wrong payment program. There are also other payments that are “pending review” that were in the right payment plan, but I have no idea why they are possibly not going to count. I cannot get anyone to tell me any information about them. I also can’t get my servicer to recertify my payments for the year. I submitted my application in February…. I love my job and want to keep working in public service, but my loans will never be paid if they are not forgiven. I am on the income-based plan, and my minimum payments are calculated as less than the interest that accrues every month. My total loan balance is going up, not down.

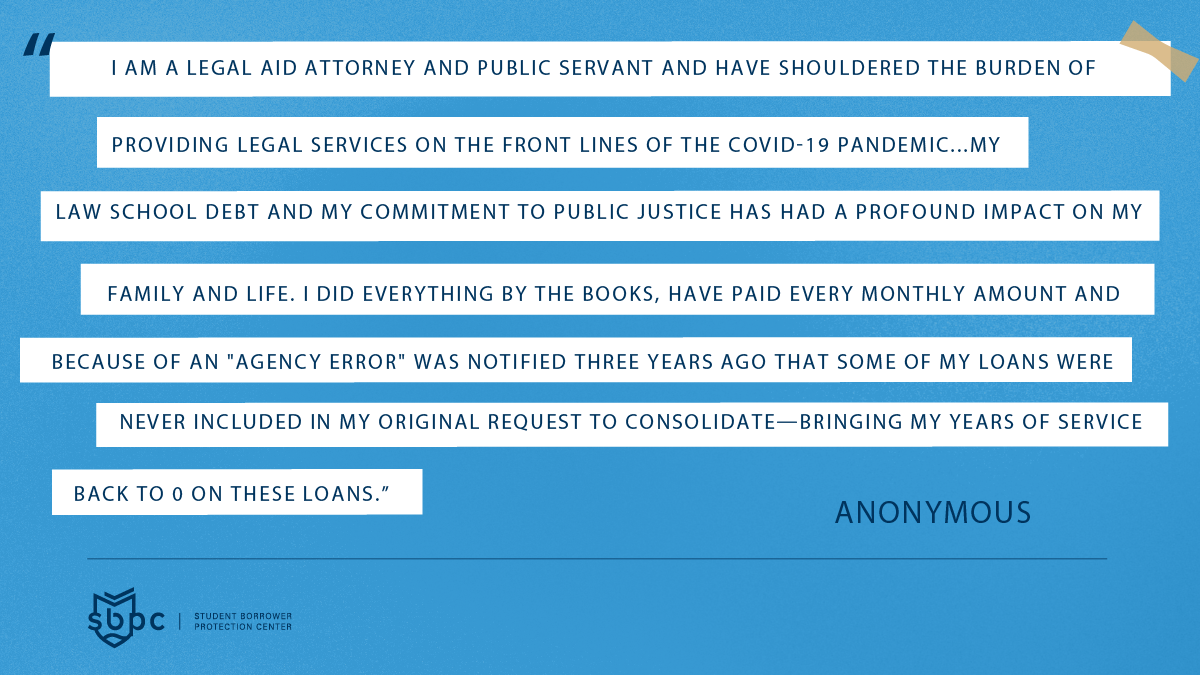

Anonymous: I am a legal aid attorney and public servant and have shouldered the burden of providing legal services on the front lines of the COVID-19 pandemic. I have risked my health and the health of my family[] to attend in-person emergency court proceedings on behalf of victims of domestic violence. I have been the[] only attorney in the courthouse, triaging cases I wasn’t assigned because literally no one was left to help those in dire need. In exchange for my commitment to public service and a salary range of about 1/4 of what my colleagues in the private sector earn, I was promised that my student debt would be erased— a promise the Biden Administration should keep. […]

I did everything by the books, [and I] have paid every monthly amount[.] [B]ecause of an “agency error”[I] was notified three years ago that some of my loans were never included in my original request to consolidate – bringing my years of service back to 0 on these loans. No one will take responsibility and no one has been able to show me documentation of this error…It feels like a trick….I earned $55,000 as a staff attorney with 8 years of seniority. We delayed having children because we couldn’t afford childcare with my salary and a house payment. Our work is so hard, meeting people at their most vulnerable, tending to them, helping them access justice.

Hollee P.: Having come from a low income family myself, and the first to graduate from college, I felt compelled to help those in poverty… In 2003, I began working for Legal Services, a legal aid organization. I left for six years to work for my state in child welfare law but then returned to my old employer. Therefore I have worked a total of 17 years in public interest. However, my loans were FFEL loans so did not qualify for forgiveness. I consolidated after graduation because I was told it would help my rate, but was talked into a 30 year repayment plan. No one told me Perkins loans could be forgiven and once I consolidated I would lose that choice. When the PLSF program began in 2007, no one informed me my loans wouldn’t qualify so I didn’t switch to direct loans until 2015. Even once I chose an income driven repayment plan that counted towards PLSF, I’m not sure if I am still on track or not as Fed Loan Servicing has not been clear with me on this issue…Meanwhile, I have spent my career working with those in poverty, and earn a very low salary by industry standards.

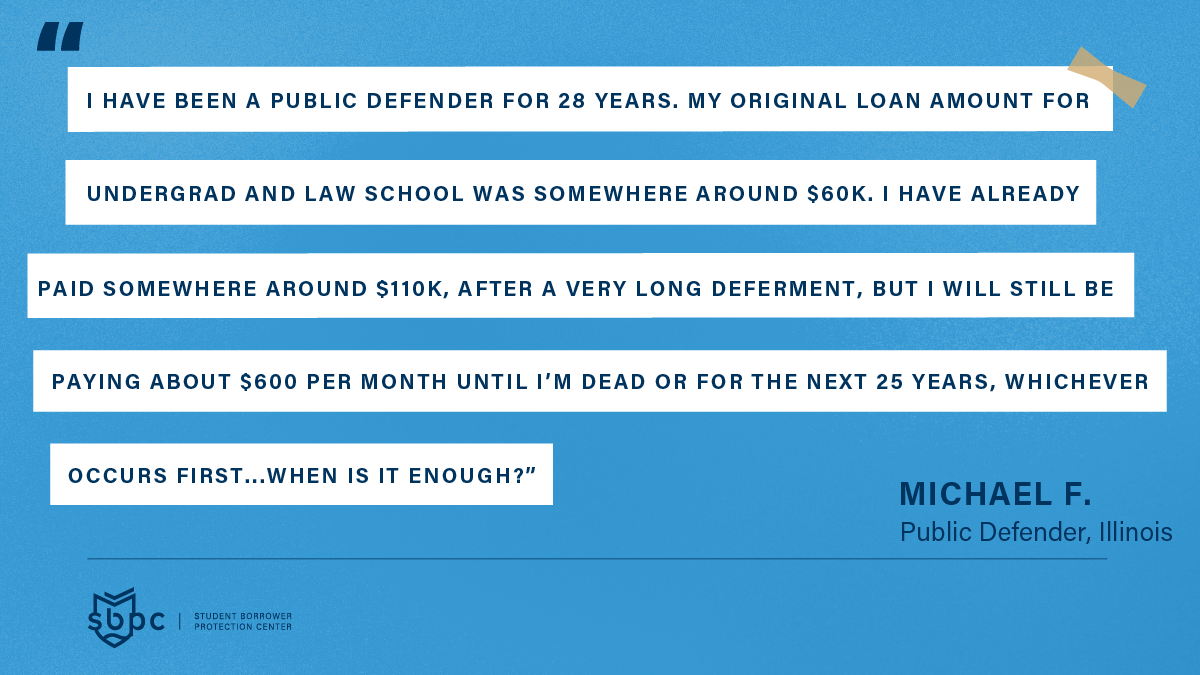

Michael F: I have been a public defender for 28 years. My original loan amount for undergrad and law school was somewhere around $60K. I have already paid somewhere around $110K, after a very long deferment, but I will still be paying about $600 per month until I’m dead or for the next 25 years, whichever occurs first. I am 57 years old. My loan provider[,] originally, Navient, never told me that I could convert my loan to a direct consolidated loan that was eligible for forgiveness. Instead, they steered me towards their in-house repayment plans. As of October 2017, I should have been eligible for full forgiveness. After submitting my certification form, I received a response saying that my loan with Navient wasn’t eligible for forgiveness. Converting to an eligible loan takes a phone call or filling out a simple form. Navient never disclosed this to me, and, as a result, I was denied forgiveness. After already paying about $110K on a $60K loan amount, I still owe $80K…When is it enough? How much in interest must I pay to be out from underneath this mountain of debt. Now, my 18 year old is heading off to college. Now, I have to finance his inflated tuition fees on top of trying to stay afloat on my student loan payments. Because our student loan debts are life-long, the financial burdens on us are compounded when our own children are leaving for college and need our financial assistance. This never ends…The cries to our government officials have been loud and unyielding, but yet nothing has been done…We need real and substantive solutions now.

Anonymous: I have dedicated my life to public service. I worked for 10 years as a 9-1-1 operator, I then attended law school. I have spent the last 14 years working for Legal Aid representing indigent citizens in domestic violence matters, public benefit matters, and landlord-tenant matters. For 14 years I have paid my student loan payment on time, every month. I have barely made a dent. Each year my organization encourages us to apply for the public service forgiveness program. Each year I check the criteria, and send an inquiry, only to be told I have the “wrong type of loan” and cannot even be considered. Whether the forgiveness program is expanded or not, I will continue to pay on time every month….At the current rate of repayment, I will struggle to have the loan paid before retirement.

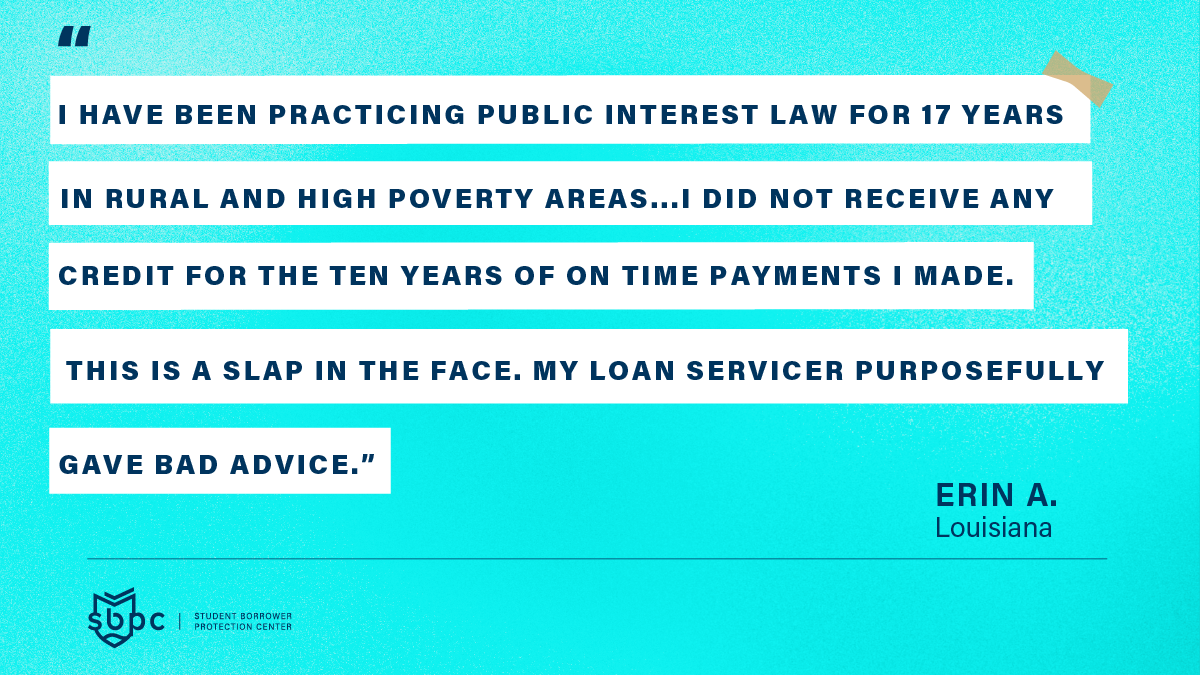

Erin A.: I was one of the first group of people to apply for public interest loan forgiveness. I have been practicing public interest law for 17 years in rural and high poverty areas[…]There was no program guidance when I graduated from law school. I waited till two years before the 10 year mark and gathered all my employer certifications, tax records, and proof of payments. My application was rejected because my loans [were] federal and consolidated but not Federal Ford Direct. All my payments were not credited despite lack of guidance or communication to borrowers from their servicers or the Department of Education.[…] I had to consolidate my loans and start paying again in 2013. I did not receive any credit for the ten years of on time payments I made. This is a slap in the face. My loan servicer purposefully gave bad advice.

Enough is enough.

Now is the time for our government to honor its commitment to those working in legal services with student loans. If you work in legal aid and have been unable to obtain PSLF cancellation or are concerned about your ability to continue working in legal aid without PSLF relief, submit a public comment to the Department now.

- Did you get insufficient or inaccurate information from your student loan company about how your older federal loan (often a FFEL loan) could become eligible for PSLF?

- Did you spend months or years in the wrong repayment plan while never being told that you needed to be in an IDR plan to qualify for PSLF?

- Did you have problems certifying that your employer was “qualified” even though you worked in public service?

- Are you one of tens of thousands of borrowers whose pursuit of PSLF was derailed by poor servicing, unfair technicalities, or for any other reason?

Your time is now. Answer the Department’s request for comment and raise your voices, share your stories, and call for President Biden and Secretary Cardona to deliver promised debt relief to student loan borrowers who have committed their careers to helping those most in need. Together, borrower stories can make a difference.

Share your story with the US Department of Education here.

###

Kyra Taylor is a staff attorney within the Student Loan Borrower Assistance Project at the National Consumer Law Center.

Kat Welbeck is the Director of Advocacy & Civil Rights Counsel at the Student Borrower Protection Center.