By Persis Yu and Abby Shafroth | December 22, 2021

In the coming weeks, tens of millions of American households will face a combination of financial catastrophes: the new Omicron variant rapidly upending our economic recovery, Congress yanking badly-needed Child Tax Credit (CTC) benefits away from working families, and the return after almost two years of debilitating monthly student loan bills. These new hardships will arrive against a backdrop of record-setting increases in the price people must pay for basic goods.

New research by the Student Borrower Protection Center and the National Consumer Law Center reveals the devastating effect that this upcoming fiscal cliff will have on households in all 50 states. In particular, our analysis indicates that unless the Biden administration changes course, student loan borrowers currently receiving monthly CTC payments will soon be forced to make an average of $400 in monthly student loan payments at the same time as they lose an average of $400 in direct financial support from the federal government. Overall, we find that without immediate action, millions of Americans will see a negative swing in their household finances averaging $800 per month.[1]

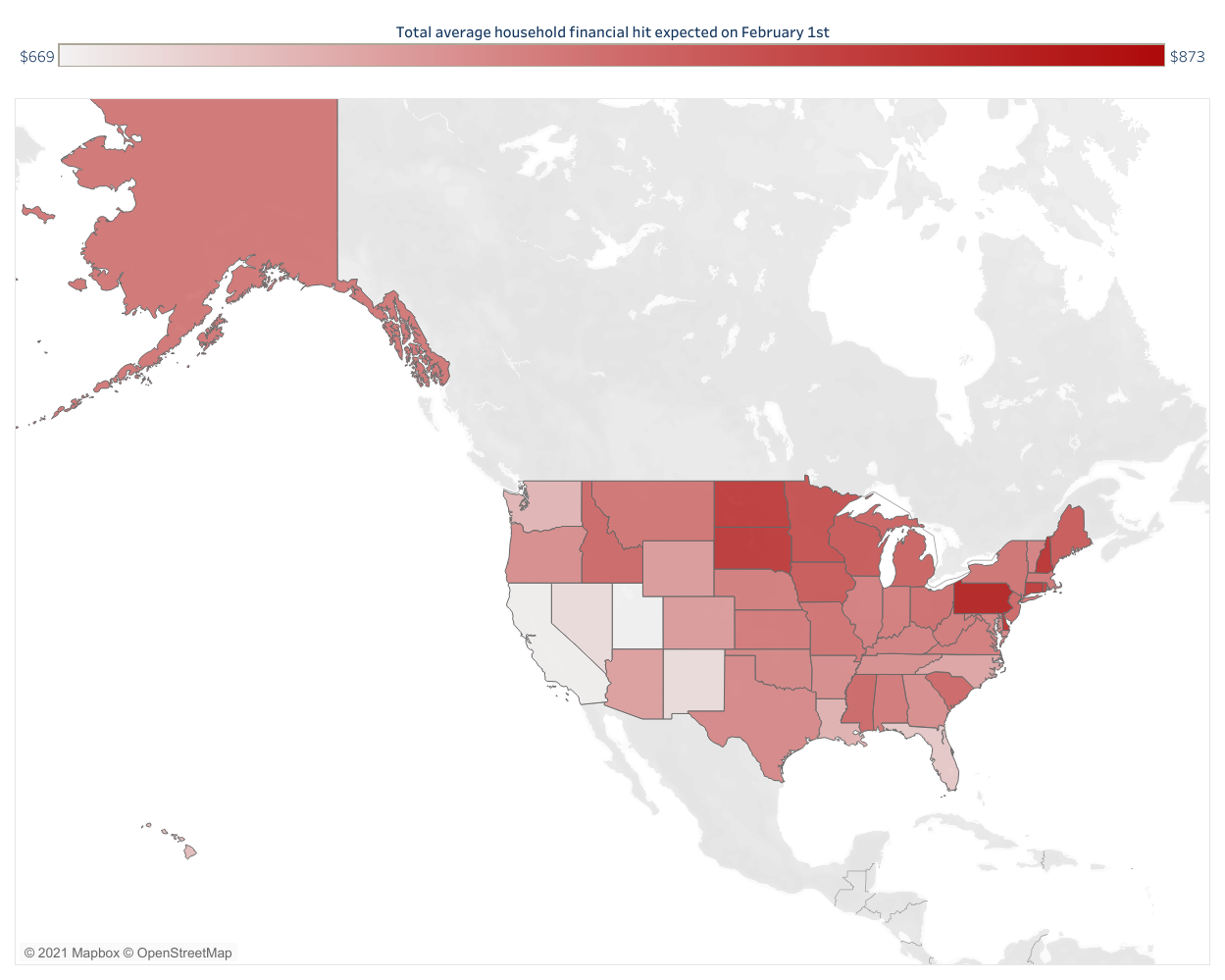

This upcoming financial shock will reach borrowers in every corner of the nation, from big cities to small towns and from the mountain West to rural communities in the East. The interactive map below shows the average budgetary swing working families will face on February 1st.

Without Action by the Biden Administration, Millions of American Families Will Lose An Average of $800 a Month in 2022

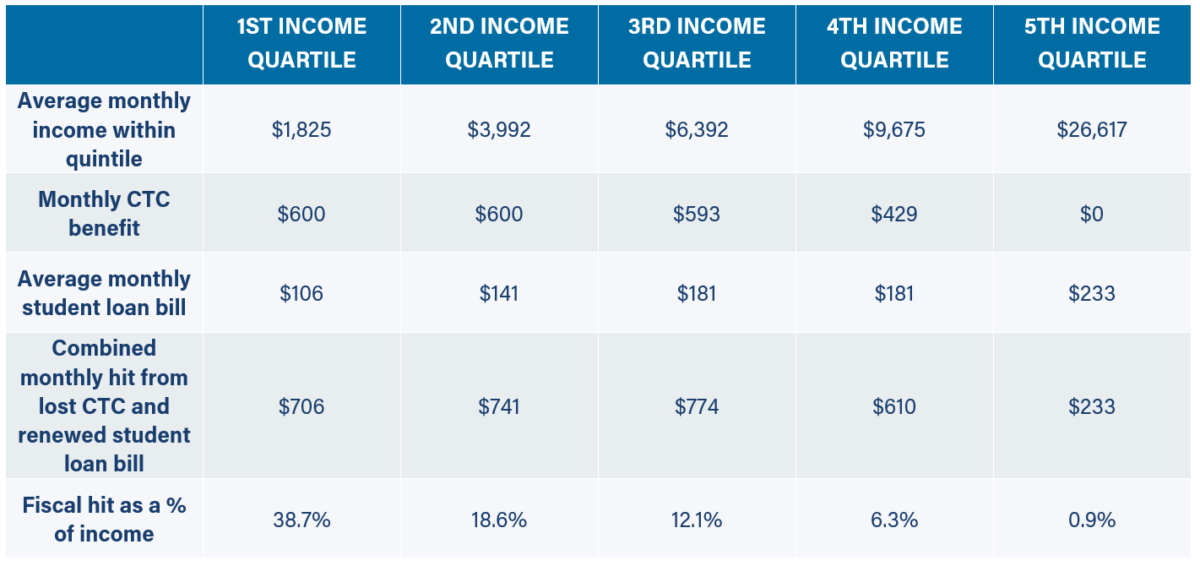

Worse, our analysis shows that this upcoming financial shock will have the largest impact on low-income households. Using public data on income levels, student loan balances, Child Tax Credit benefits, and more, we compared how the combination of lost CTC benefits and resumed student loan payments will affect Americans across the income distribution. We found that the upcoming financial cliff will cost the lowest income households an amount equal to more than 38 percent of their income, while it will cost the highest income households an amount equal to less than one percent of their income.[2]

The Biden Administration Has to Act Before It’s Too Late to Prevent Financial Devastation

Our state-by-state analysis comes on the same day that Fighting Chance for Families released a new poll revealing that almost half of borrowers have no confidence in their ability to make student loan payments should the Biden administration restart payments in February 2022 as planned. This sentiment cut across party lines, being voiced by pluralities of Democrats and Republicans and a majority of independents. At the same time, fewer than 1-in-7 people with student debt reported being “very confident” in their ability to make student loan payments when they come due.

The data is clear: restarting student loan payments while allowing CTC payments to expire is a kick in the teeth to all working American households. Allowing these costs to coincide as planned will harm millions, particularly those already in the most difficult financial positions, as the omicron variant threatens our already fragile economic recovery. And this is before even considering the massive operational breakdowns that borrowers are already grappling with as they prepare to return to repayment.

COVID-19 is completely indifferent to borrowers’ finances, to the necessity of support for working families, or the massive burden that student loan debt places on Americans. The Biden administration must choose not to be indifferent.

###

Persis Yu was the Policy Director and Managing Counsel at the Student Borrower Protection Center. Persis is a nationally recognized expert on student loan law and has over a decade of hands-on experience representing student loan borrowers.

Abby Shafroth is a staff attorney at the National Consumer Law Center and focuses on student loan and for-profit school issues.

Have you lost your Earned Income Tax Credits or Child Tax Credits because of federal loans in default? Please share your story with us here.

[1] SBPC calculations based on Student Loan Planner and the Department of the Treasury. Considers only households with student loans that received monthly CTC benefits, and assumes for simplicity that their average student loan payment and CTC benefit reflects that of the public as a whole. Given that these borrowers are likely lower-income, making it likely they would qualify for relatively larger CTC benefits and be more reliant on student loans, the above estimates are likely conservative relative to the true financial hit these borrowers face.

[2] SBPC calculations based on the Congressional Budget Office, the Washington Post, People’s Policy Project, and the Education Data Initiative. Assumes 10 years remaining in repayment at the restart point. Assumes 10 years remaining in repayment at the restart point. Assumes a single head of household with two children under 6.

**The full blog post is available at https://protectborrowers.org/if-payments-resume-and-child-tax-credit-benefits-expire-february-1st-will-mark-a-fiscal-cliff-for-millions-of-households-in-all-50-states/